What is the 40 30 20 10 rule for money?

The most common way to use the 40-30-20-10 rule is to assign 40% of your income — after taxes — to necessities such as food and housing, 30% to discretionary spending, 20% to savings or paying off debt and 10% to charitable giving or meeting financial goals.

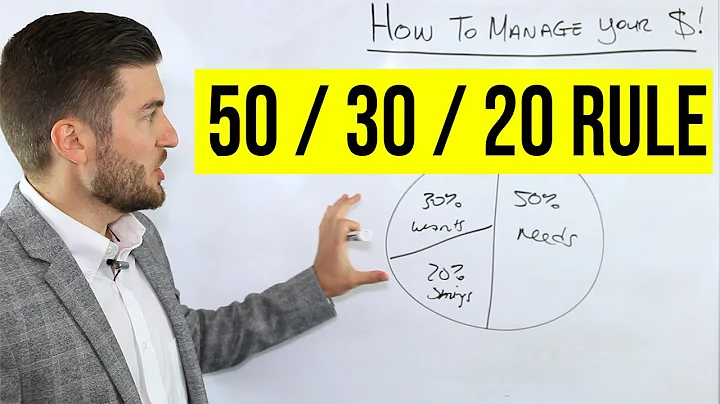

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals. Let's take a closer look at each category.

The 40–40–20 budget rule is a simple yet powerful guideline that allocates income into three distinct categories: 40% for necessities, 40% for savings and debt repayment, and 20% for discretionary spending.

The 70-20-10 budget formula divides your after-tax income into three buckets: 70% for living expenses, 20% for savings and debt, and 10% for additional savings and donations. By allocating your available income into these three distinct categories, you can better manage your money on a daily basis.

The rule requires that you divide after-tax income into two categories: savings and everything else. So long as 20% of your income is used to pay yourself first, you're free to spend the remaining 80% on needs and wants. That's it. No expense categories.

Drawbacks of the 50/30/20 rule: Lacks detail. May not help individuals isolate specific areas of overspending. Doesn't fit everyone's needs, particularly those with aggressive savings or debt-repayment goals.

However, one of the most important benefits of this rule is that you can keep more of your income and save. The 20/10 rule follows the logic that no more than 20% of your annual net income should be spent on consumer debt and no more than 10% of your monthly net income should be used to pay debt repayments.

Put 60% of your income towards your needs (including debts), 20% towards your wants, and 20% towards your savings. Once you've been able to pay down your debt, consider revising your budget to put that extra 10% towards savings.

The 80/20 rule says that you should first set aside 20% of your net income for saving and paying down debt. Then split up the additional 80% between needs and wants. When using the 80/20 rule, calculate the amounts based on your net income - everything leftover after you pay taxes.

The seven percent savings rule provides a simple yet powerful guideline—save seven percent of your gross income before any taxes or other deductions come out of your paycheck. Saving at this level can help you make continuous progress towards your financial goals through the inevitable ups and downs of life.

What is the #1 rule of budgeting?

The idea is to divide your income into three categories, spending 50% on needs, 30% on wants, and 20% on savings. Learn more about the 50/30/20 budget rule and if it's right for you.

When following the 10-10-80 rule, you take your income and divide it into three parts: 10% goes into your savings, and the other 10% is given away, either as charitable donations or to help others. The remaining 80% is yours to live on, and you can spend it on bills, groceries, Netflix subscriptions, etc.

If the 50/30/20 budget was once considered the golden standard of budgeting, it's not anymore. But there are budgeting methods out there that can help you reach your financial goals. Here are some expert-recommended alternatives to the 50/30/20.

The 90–10 rule refers to a U.S. regulation that governs for-profit higher education. It caps the percentage of revenue that a proprietary school can receive from federal financial aid sources at 90%; the other 10% of revenue must come from alternative sources.

This rule suggests that 80% of effects come from 20% of causes. For example, 80% of a company's revenue may come from 20% of its customers, or 80% of a person's productivity may come from 20% of their work. This principle can be applied to many areas, including productivity for small business owners.

Key Takeaways

With the 80/20 rule of thumb for budgeting, you put 20% of your take-home pay into savings. The remaining 80% is for spending. It's a simplified version of the 50/30/20 rule of thumb, which allocates 50% of your take-home pay to needs, 30% to wants, and 20% to saving.

When you pay yourself first, you pay yourself (usually via automatic savings) before you do any other spending. In other words, you are prioritizing your long-term financial health.

At least 20% of your income should go towards savings. Meanwhile, another 50% (maximum) should go toward necessities, while 30% goes toward discretionary items. This is called the 50/30/20 rule of thumb, and it provides a quick and easy way for you to budget your money.

The 30% Rule Is Outdated

To start, averages, by definition, do not take into account the huge variations in what individuals do. Second, the financial obligations of today are vastly different than they were when the 30% rule was created.

The factors that determine your credit score are called The Three C's of Credit – Character, Capital and Capacity.

What are the 5 C's of credit?

Called the five Cs of credit, they include capacity, capital, conditions, character, and collateral. There is no regulatory standard that requires the use of the five Cs of credit, but the majority of lenders review most of this information prior to allowing a borrower to take on debt.

Character, capital (or collateral), and capacity make up the three C's of credit. Credit history, sufficient finances for repayment, and collateral are all factors in establishing credit.

The 25x rule entails saving 25 times an investor's planned annual expenses for retirement. Originating from the 4% rule, the 25x rule simplifies retirement planning by focusing on portfolio size.

How about this instead—the 50/15/5 rule? It's our simple guideline for saving and spending: Aim to allocate no more than 50% of take-home pay to essential expenses, save 15% of pretax income for retirement savings, and keep 5% of take-home pay for short-term savings.

50 - Consider allocating no more than 50 percent of take-home pay to essential expenses. 15 - Try to save 15 percent of pretax income (including employer contributions) for retirement. 5 - Save for the unexpected by keeping 5 percent of take-home pay in short-term savings for unplanned expenses.